Last Updated on April 9, 2021 by The Young Firm

A Jones Act settlement doesn’t just happen. It takes experts, medical testing, documents and leverage to get a fair settlement. Because settling a maritime injury claim is a potentially complicated process, it should not be taken lightly or done without preparation. This webinar walks you through the process and discusses the main pitfalls to watch out for. This webinar covers the following:

10 Key Points When Negotiating a Jones Act Settlement Amount

- Never make the first offer

- Have them make an offer in writing

- Have them break down what they’re offering you

- Don’t settle without knowing the full value of your case

- Think about what the best alternative is for you and for them if you don’t settle. What could happen to you versus what would happen to them?

- Waiting as long as possible to settle your claim benefits them and hurts you

- They will not make a fair offer unless they have to. No one pays their bills before they’re due.

- Without medical tests, experts, and other important documents, you won’t be able to prove your case

- Test the company’s honesty by asking for key documents (witness statements, recorded statements, accident reports, etc.)

- Louisiana attorneys can help pay for your medicals and the experts needed to build a good case

Keep Detailed Records

Keep records of all conversations with the insurance company, including details such as:

- The date and time of the conversation

- The adjuster’s questions

- Your answers to the questions

- Any other topics discussed during the conversation

Watch the full video or read the transcript for more tips on what to look out for if you’re planning to settle your own. Finally, call us if you have any questions about how you should move forward.

Webinar Outline

- About Us

- Basic Negotiation Points

- Best Alternative to a Negotiated Agreement (BATNA)

- Understanding Your Medical Condition

- Collecting Accident Reports

- Getting a Fair Offer

- How to Test the Company’s Honesty

- The Best Practices for Settling a Claim

- What the Benefits Are Of Hiring an Attorney for Your Claim

Webinar Transcription

[0:01]: Hello. In today’s webinar, we are going to cover do-it-yourself Jones Act settlements. We’re going to go through whether these are a smart move to try to save you money as an injured maritime worker trying to settle his own case, or whether it may be a bad idea to try to settle your own case, and whether you may be leaving a lot of money on the table.

[0:19]: Now specifically, this webinar is going to discuss the concepts and the ideas of an injured maritime worker under the Jones Act, or even maritime law, trying to settle his own claim without an attorney.

[0:33]: We’re going to go through some of the potential pluses, we’re going to go through some of the potential downfalls. And I’m actually going to give very specific suggestions and observations about best practices and what we feel is a really good practice if an individual is going to try to make any type of settlement discussions at all on his own without an attorney.

About Us

[0:53]: Now, let’s go through a couple of points here before we start. First, my name is Tim Young. I’m your host. I’m a maritime attorney from New Orleans, Louisiana. We have a Gulf Coast practice here – it’s actually a national practice primarily along the Gulf Coast. For more than 23 years I’ve been handling maritime and Jones Act cases for injured workers, basically throughout the nation – throughout the United States – with a real focus on Louisiana, Texas, Mississippi, Alabama and Florida.

[1:24]: We have successfully helped (myself and my law firm) we’ve successfully helped clients with very serious injuries – multiple brain injuries for clients, major burns, multiple surgeries. We’ve really been honored and – frankly honored – to play an important part in their lives trying to piece things back together for them after very serious injuries.

Negotiating Injury Settlements

[1:48]: Let me go through some basic ideas here about the Jones Act or about negotiations first. What we’re going to discuss here are basic negotiation points. And these are two points that I want to bring up, and they both go to:

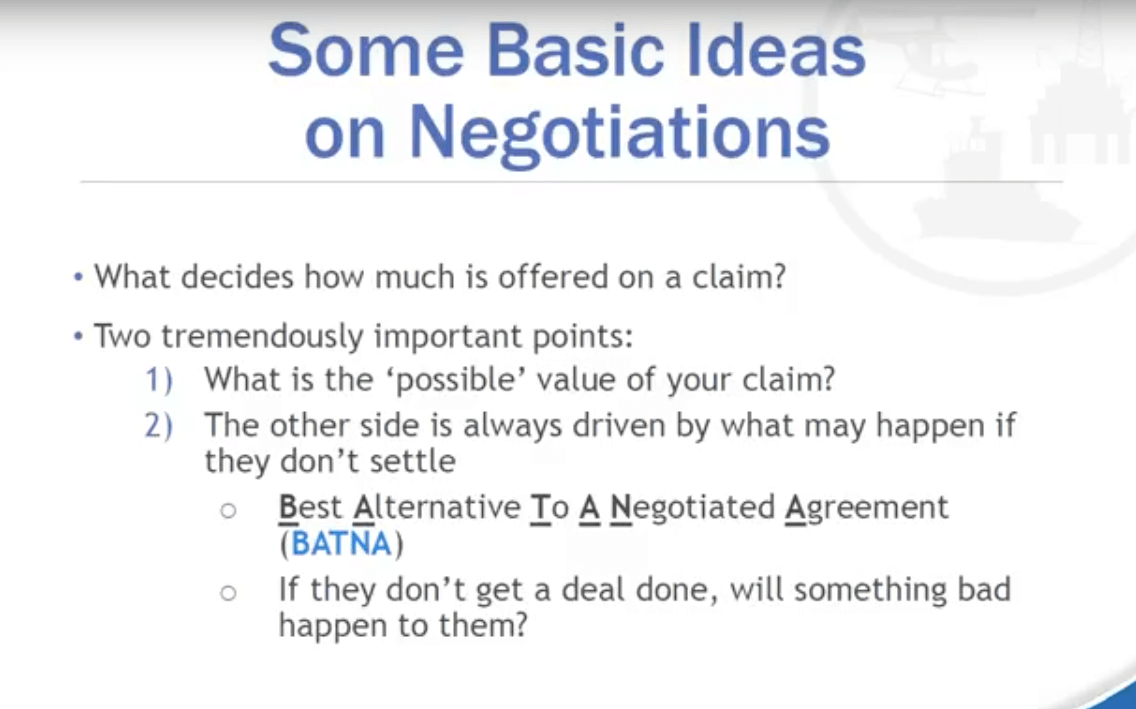

[2:01]: What decides how much is offered on a claim? So we want to start today with the basic idea of, overall, what decides when a party sits down at a table – What generally decides how much is going to be offered when they’re trying to negotiate something? There are two tremendously important points here. These are the two core concepts I really would ask you to try to understand.

[2:26]: There will be a download at the end of this webinar. It will have these points on it. I think they’ll be helpful to you as you try to move forward thinking about your position and when you try to negotiate.

[2:37]: The two most important points when you’re trying to negotiate. One of them is: What is the possible value of your claim?

The Possible Value of Your Claim Determines How Much They’ll Offer

[2:45]: What this refers to is the party on the other side of the table from you, they are going to be thinking – this is one of the most important ideas going through their head – “What is the possible value of your claim? What is the highest amount that your claim could potentially be worth?” Because that is going to anchor how they start to make offers, and how they what they call “evaluate your claim.”

[3:10]: The second very – well let’s break this down a little bit first – Is the claim potentially worth a dollar or $1,000,000? And the difference obviously is if it’s a claim that at the most could be worth a dollar that is going to anchor and drive how much is offered to you. If it is a claim that potentially could be worth $1,000,000, obviously that drives the amounts that are going to be offered to you.

What Will Happen if They Don’t Settle?

[3:34]: The next important point here (it’s item number two on the slide) is that the other side is always driven by what may happen if they don’t settle. And this is a very important concept. The other side sitting across the table from you will always be thinking in their head: “If we leave here without getting a deal done, what does that mean for us? How does our next week look? How does our next 30 days look? What type of a short-term future are we going to have if we don’t get a deal done?”

BATNA

[4:02]: This is actually referred to – it’s so important of a point in negotiation – it’s referred to as the Best Alternative to a Negotiated Agreement. A “B-A-T-N-A.” That’s just a fancy term that negotiators, professional negotiators, have come up with for this concept. Let me give you some examples here of how this plays out in the real world.

[4:23]: Again like I said, if they don’t get a deal done will something bad happen to them? That’s another good way to think of it. If they leave the table, are they going to have an adverse effect when they leave the table? Or things going to stay the same for them or potentially even get better? Which I’ll give some examples of in a second. This is one quick example here:

Example: Buying a New Car When Your Existing One is Broken

[4:42]: If you have a broken-down car and you push it into a car dealership, and you’re trying to negotiate for the purchase of that new car, you do not have a very good BATNA. You don’t have a very good alternative if you can’t negotiate a new car, and the dealer will know that. And they’ll know that essentially when you leave that parking lot – that car lot – you will have to figure out transportation. You may have to go to another sales place to try to negotiate. Start all over again for a new car. So the dealer kind of has you in a bad spot. And everybody kind of knows this intuitively when you go and try to negotiate for something that you just have to have. Well, what’s going on behind the scenes is, you don’t have a very good alternative if you don’t get the deal done. “You really need the deal,” is how people say it.

Example: Moving into a New Place After Selling Your House

[5:29]: Another quick example is sometimes people will get a really good offer for their house and they go and sell it quickly. And then they’re forced in the next thirty or sixty days to try to go find another place to live. When they go negotiate and they go look at other places to live – maybe it’s a house, maybe it’s an apartment they’re going to rent – again, they don’t have a good alternative if they don’t get that deal done. Because they’ve sold their house. They’re going to be on the street. They have to get a deal done. They’re eager for it.

[5:54]: What is going on, again, psychologically is you really don’t have a good alternative to getting a negotiated agreement. So, that’s the second core principle here. Again just to recap, a fundamental critical point is: What is the possible highest value of a claim? The second fundamental point is: What does the future of that party look like if they don’t get a deal done?

Your BATNA vs Theirs

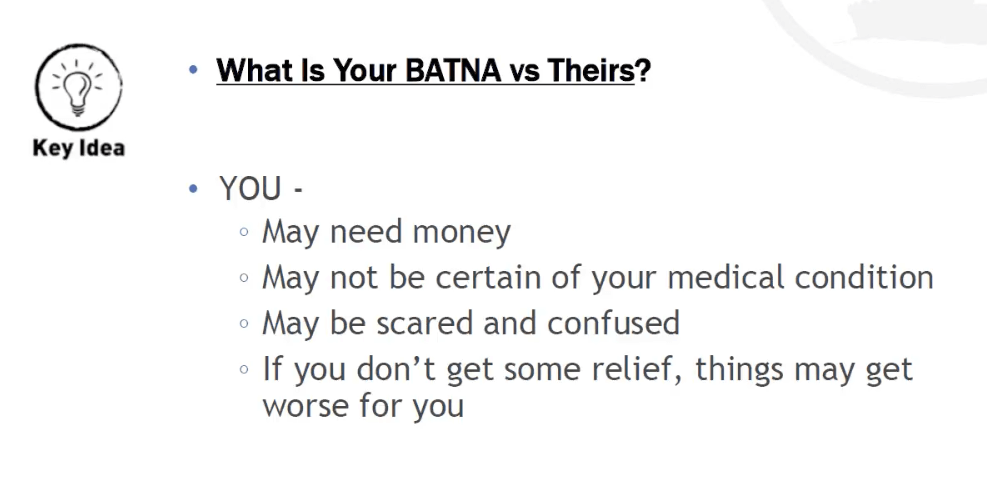

[6:18]: Let’s go through some key ideas here. This is going back to BATNA, and it’s basically “What is your BATNA versus their BATNA?” And this is more specific to a Jones Act situation – individuals that have been injured working on a vessel. What is the alternative for that individual when they sit down and even think about discussing a settlement of their case without an attorney or without filing any claim?

[6:42]: Same thing on their side. What does their alternative look like when they’re sitting down with an unrepresented seaman trying to negotiate a maritime claim for somebody who doesn’t have a lawyer?

You Need the Money

[6:55]: You have a situation where potentially you may need the money. A lot of times – all of our clients go through very, very tough times – a lot of times they’re not getting paid what they used to earn. Their bills are starting to slowly pile up. They’re getting behind a little each month. So when they go into any type of settlement discussions, typically it’s a financial crisis. They really need money.

You Don’t Know Your Full Medical Condition

[7:18]: Next one is they may not be very certain of your medical condition. You may not be when you try to negotiate this. A lot of times companies will be reluctant to approve a lot of testing, so you may not know the real – the real – severity of your injury. Or sometimes parts of our clients, parts of the bodies, haven’t even been checked out yet. We see that a lot – people call us and say, “My back got hurt also, but they’ve never sent me to a doctor for that.”

You’re Scared and Confused

[7:48]: A lot of times, frankly, you’re going to be scared and confused. You really don’t know going in this type of process if you’re doing anything right or wrong because you really haven’t done it before.

Things May Get Worse for You

[7:58]: Bottom line here, and this is the last point, is if you don’t get some type of relief when you go into some type of settlement discussion with your company after your injury, things may get worse for you.

Nothing Bad Really Happens to Them

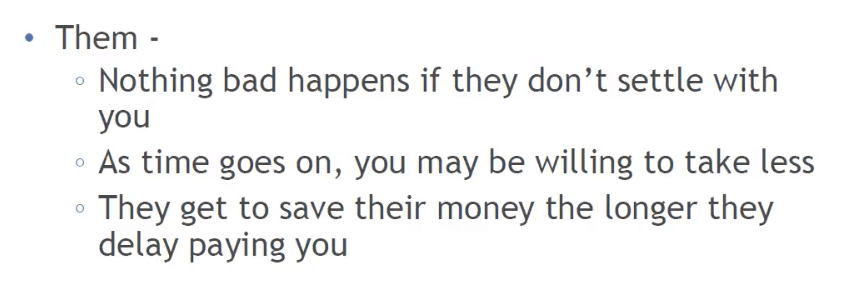

[8:09]: Let’s look at it from their point of view now. From their point of view, really nothing bad happens to them if they don’t settle with you. This is again if you’re unrepresented. There’s no claim filed in court. And they’re doing – we see this all the time – the client, the injured maritime worker/seamen will basically have a lot of treatment, a lot of times they have surgeries done, and then the company will call up and say “OK, it’s time for our insurance person to come out. We want to sort of settle up with you. We want to talk about wrapping all this up, maybe get you back to work.” That’s the language they use a lot of times. Well, what’s going on is: They come out, they meet with you, maybe they do it by phone. And if they don’t get a deal done, nothing bad really happens to them. Their next week looks pretty much like their last week did.

It Benefits Them to Wait it Out

[8:55]: As time goes on – this is a second point here – they may, you may actually be willing to take less. So they may get in a better position as time goes on because you get more desperate. And the third point here is: They really get to save their money the longer they get to delay paying you.

You Don’t Pay Your Bills Early, Neither Will Your Company

[9:12]: A lot of times I’ll use an example of people getting electric bills and rent bills. People don’t send their money in early. Usually, they wait on those bills until they’re actually due. A little bit of the same concept there where the company is thinking “There’s really no urgency to settle this man’s claim. We get to hold on to our money longer unless he gives us a really good incentive and a really good kind of a quote good deal on their end for settling it.” Whatever number that you’re willing to take.

[9:40]: Let’s go through a couple of things to think about before you even think about settling or discussing the settlement of your own Jones Act case or maritime case. These are just some points I want to walk through quickly and see, as you kind of going through this checklist, think if you’ve gone through these and if these – if you’ve kind of satisfied these, or some of these are kind of outstanding and still lingering in your situation.

Understanding Your Medical Condition

[10:06]: First one is – Do you have an accurate understanding of your medical condition? This is very important. Multiple – many, many, many times it is more common than not for an individual who’s been injured offshore to call us. Maybe they got hurt on a tugboat or a barge. They call us, they’re obviously very scared. But always, almost always, we hear that one of their real concerns is their medical condition. They’re not positive they’re getting the right treatment. But like I mentioned earlier, sometimes they haven’t had parts of their body examined properly or tests run on certain parts of their body to figure out what’s going on. So the first question here is: Do you really have a 100% full accurate view of your medical condition and all your injuries? Have you had all the tests done?

Is Your Doctor Trustworthy?

[10:55]: A couple of items here to go through this: Do you have an opinion from an honest doctor that you picked? Again, it is more common than not that companies or insurance adjusters will get injured maritime workers to their own doctors that they pick. A lot of times it’s not somebody that you really trust or have a relationship with before your injury.

Did You Get All the Proper Testing Done?

[11:13]: Next one is: Have you had all the necessary testing done? You know I mentioned this a second ago – this is sort of a checklist here. Have you had MRIs done? Have you had CTs done? Have you had nerve conduction? A lot of times things can manifest as sort of a tingling or a burning sensation and that could actually be nerve damage. There are tests that can try to identify that for you. And a lot of times, companies or insurance companies are not going to want to spend money on a test. Because number one – it costs them money. More money out of their pocket.

[11:43]: More importantly though, and this is important to understand is, if they go and pay for a test, and it shows that you do have nerve damage or a bad disk or some type of injury that needs to be fixed. What they’ve then done is, they went out and they spent their own money and they now have evidence and proof that you need more treatment and that you’re more seriously hurt than they thought. So it really doesn’t make sense from their point of view to be funding a lot of that and moving that forward for you. From your point of view, that’s critical information that you’ve got to know though. So that’s a real conflict going on right there with the situation.

Do You Know the Full Cost of Any Future Medical Treatment?

[12:21]: The last item here, third item here, is: Do you know the full cost of any future treatment? This is going to be very important and you’ll see in a few minutes why. But have you talked to, again, honest doctors that you pick to have had all the testing done that they want to do and have they talked about whether you need any type of procedure? Maybe you don’t want it done right now. Or this year. Or next year. But at some point in your future, are you going to need to have a serious surgery that may cost $100,000 or $150,000? You’ve got to figure all that out really before you can sit down and get a real idea of what your potential claim may be worth.

What are You Physically Capable of Doing?

[13:02]: Last one here is: Do you know what you are physically – what you are actually physically capable of doing after your injury? It’s the last one here. I’ll read it again for you. Do you know what you actually are physically capable of doing after your injury?

[13:18]: This is very, very important. A lot of our clients and potential clients have obviously been off work after an injury. They have not been back to full-duty work. They assume that they can go do heavy work. They’re not positive, and so they’re really in a position of lack of knowledge there.

Test Their Honesty

[13:36]: One suggestion moving on here is to test the insurance company’s honesty to you – with you – before you began. What I mean by this is – and I’m going to give you some real specific tips here on how to do this – but you want to test their honesty. They’re going to come into this situation with you and basically say, “All right, we want to try to wrap things up. You’ve had treatment now, maybe you’ve had a surgery or two, even. You haven’t been at work for a while. Let’s go ahead and settle things up. Let’s square things up.” And they typically approach you with this concept or this idea. So a real belief here, our office really believes you should test their honesty before you even start this process. If they’re being genuine with you, then when you walk through these next points, you’ll figure that out pretty quickly.

Ask for Key Documents

[14:24]: The first one is to ask for all the key documents that they already have and you don’t. And this is pretty basic, but if you step back from your situation – and it’s hard because it’s very emotional and you’re really in a strange, different place. But if you step back and you think about this, they have on their boat, or in their company, or in their rig, or wherever the injury occurred, somewhere they have a file with a bunch of stuff in it. And a lot of times, it’s key documents that they have that you don’t. And you don’t know what any of those say. And those are going to be important as I’ll explain.

Witness Statements

[14:56]: So first one is you want to ask for the witness statements. And again, there’s a checklist you can download at the end of this webinar. But you want to ask for witness statements. Perhaps when your injury or accident happened, the company went out and talked to a bunch of the coworkers – your coworkers – who were standing nearby. Maybe even, you know, people who witnessed it and they may have written up favorable stuff about how it happened that helps you.Accident Report

[15:20]: Next thing you want to ask for the accident reports. Pretty basic, but you want to see what they wrote on them. A lot of times our clients are seriously injured and they’re really not familiar with what was put on the accident report. They get airlifted off the rig or they get brought from the doctor immediately to the emergency room so they really don’t know what those reports said. You want to ask for copies of those. Again they have these things, and if you want an equal footing, if you want to balance negotiation here, you want to have the information that they have before you even start this process.

Recorded Statements

[15:51]: Next thing you want to ask for your recorded statement. A lot of times companies will have called you – again I can’t tell you how many times our clients or potential clients call and say, “You know, I gave something I don’t remember well. It was in the hospital. The guy came out a day after the injury. I was on medication.” – and you want to ask for that. Because that may have good information there where you really explain what happened well or it may have bad information that hurt you but you want to know that.

Investigation Reports

[16:19]: Very important here, number four here is you want to ask for the investigation reports. These are a little bit different than accident reports, and a lot of you guys who’ve been out there for a long time know this. These kinds of reports – “root cause analysis” is what they call them. Sort of “investigation reports” is what they’ll call them. Sometimes even to a PowerPoint slide where they walk through what happened and why it happened, and how to prevent it. That is going to give you the fault part of the case – the negligence. The “what happened that shouldn’t have happened” part. And you do want to know that before you get into any type of discussion about what they may owe you.

Know How Fair They’re Being

[16:56]: So here again is, you need to really know how fair they’re being with you. You need to know how fair they’re really being with you before you even start dealing with them. That’s a strong suggestion of ours. Just a good basic rule with any type of negotiation, especially when it’s one involving an injured maritime worker who may not have experience with this going up against a real seasoned insurance adjuster who does this all the time for a living. So from the get-go, you want to get a real idea of “How fair is this guy being?”

Being Nice Isn’t the Same as Being Fair

[17:28]: Another thing I cannot tell you how many times happens is our clients, or people who end up becoming our clients, will say that they dealt with the adjuster. “Overall he was a nice guy you know, I kind of trusted him. I thought he was fair.” And a lot of adjusters – they are nice, you know. But they’re doing their job at the end of the day. And what happens is, when you really drill down and you ask for these documents you’re going to figure out pretty quickly if he is really showing you all his cards. Or if he’s trying to, you know, use very nice friendly language but at the end of the day is not giving you the same information they have access to.

Settling Your Claim Without an Attorney: Best Practices

Legal Disclosure

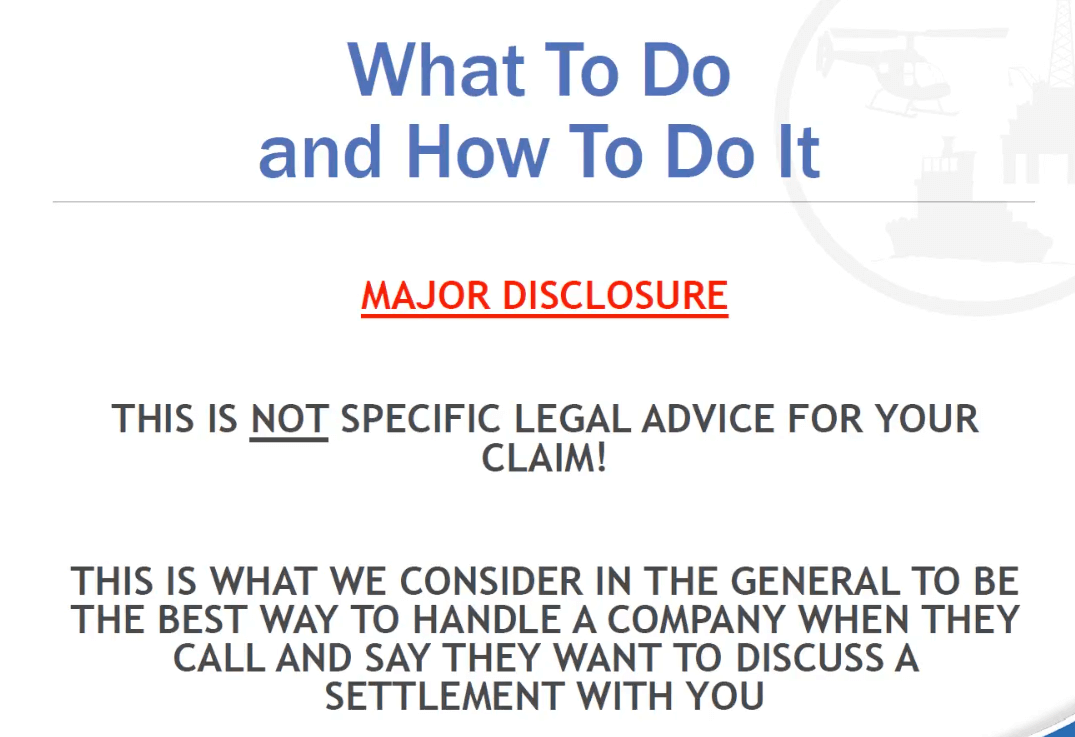

[18:05]: Let’s get down to it. Let’s get down to sort of some observations we have as to what to do and how to do it if you’re even thinking about discussing settlement with your own Jones Act case without an attorney. Now the first thing is major disclosure here. Obviously, I am an attorney. I’ve done this for more than 23 years. Major disclosure though is that this is not specific legal advice for your claim. If you’re watching this webinar, chances are we haven’t talked yet. We’re happy to speak with you at any point but until we know the specifics of your case, we really cannot give you specific advice. What I’m going through here is general concepts on what we consider to be best practices.

The best way to handle a company when they call pretty much anyone and ask to discuss settlement. So again this may not necessarily apply in your case. But in general, these are what we believe are very strong good concepts. Hopefully which you might be able to do is sort of apply them to your situation. Again, please call us if you have any questions about your specific situation. We’re happy to talk with you at no charge at all. But again, I do need to let you know that these may not actually apply to your situation, but they’ll certainly give you something to think about.

Tell Them to Make You the Best Possible Offer

[19:23]: Going through here, first step – this is what we always recommend to somebody that calls us and says, “You know the company’s talking with me, what do I do?” Tell them to make the best possible offer to you. Tell them to make the best offer possible to you. They are approaching you, they understand the value of your case (or they should), and they should be the ones who make the first offer out there to you.

Get it in Writing

[19:47]: So number one here. This is again drilling down a little bit more detail on this concept. Tells them to put the offer in writing – get it in writing there. Again, very common. I don’t want to say “trick,” but a very common practice is they may mention one amount and talk about this. Stuff on phones these days, people may not remember. A lot of times people say, “Oh you might have heard something different. You must’ve misunderstood me.” So the best way to do it is in writing. It’s so easy now to text or email each other. Just say “Put it in writing what you’re going to offer me.”

Break it Down

[20:21]: Second point here, this is important, is to tell them to break it down for you. Why are they offering you that amount? How much is for wages? How much is for pain? You want a line-item checklist on what the $25,000, $50,000, maybe $100,000 offer is based on. And if they, the more general they are with it, the more that should be a red flag for you. If they’re saying, “Well it’s just an offer it’s what we think overall is good.” Because you want to know.

[20:50]: Maybe you’ve lost six months of wages and you want to know where they even considering that. Maybe you’ve had two surgeries and they’re going to offer you an amount that really is basically just your wages. You want to know – are you all even paying for my pain. And if they’re honest and they say, “No we’re not,” it’s important because then you can ask why not. And maybe they have a good explanation. Maybe, I don’t know what their reason would be. But at least you have the ability to intelligently discuss what they’ve offered you.

Never Start Negotiations with an Offer: Don’t Give Them a Number

[21:21]: Second point here is under no circumstances – and this sort of goes back to the first point – do not start negotiations by giving them a number. Under no circumstances should you make the first offer. There’s a saying by the legendary investor Warren Buffett. He says, “Rule number one is: Don’t lose money when you make an investment. Rule number two is: Never forget rule number one.” And this is kind of the same situation for anybody sitting down trying to talk to a seasoned professional insurance negotiating adjuster, or a company that handles claims all the time. What you want to do is tell them to make the first offer. And you never want to forget that first rule.

Why You Should Never Make the First Offer

[22:05]: A couple of reasons why, and I want to explain this. I don’t just want you to take it on trust, here. Hopefully, you’ll understand the process better as we go through these. The first one is: If you make the first offer, you’re going to be setting a baseline. And any negotiations that occur, the first offer is very important. And that’s a longer detailed discussion on psychology and everything else, but that first offer is very important. So you’re going to be setting some type of baseline.

Your Offer Goes on File Forever

[22:31]: The problem with any baseline here is number one is it’s going to go into the insurance companies file forever. Many, many times, clients have hired us after having some discussions with the company. Maybe they indicated, “Look you know I’m trying to be really fair. I worked with you all for 15 years. If you just pay me X amount, we’ll be happy. I can get back on my feet. I think that’s fair.” Well, the company will then say, “Eh, we’re sorry we can’t do that. We’ll offer you a third of X.” And the client gets very upset, storms out of the conversations or you know breaks ways with the company, hires us. It is amazing. Nine months down the road when we’ve been involved and everything has changed, and maybe the clients even had another surgery at some point, they inevitably bring up that X number. And they say, “Well you know before your client hired you, he was willing to take X amount. So we’re going to kind of start negotiations around there.” And it just digs a hole that you really have trouble getting out of later.

They’ll Offer Less Than What You Initially Ask For

[23:32]: The second point here is they’re naturally going to offer you a lot less. Your idea of making an offer of a fair number really can backfire on you. The third idea here is if your condition changes that number still out there. A little bit of what I said a moment ago. Things can change but at the end of the day you can’t let the horse – that horse is out of the barn. As they say, it’s basically a done deal. You’ve got it down there in your file and you’re going to be having to explain it or trying to work against it down the road.

What You Don’t Know Can Hurt You

[24:06]: Second point here on why you should never make the first offer is what you don’t know can hurt you tremendously. Sometimes people say the opposite. I don’t believe that’s true. What you don’t know can actually hurt you very badly. I’m going to give you some examples here.

You Won’t Have a Formal Wage Loss Report

[24:24]: When you are unrepresented, and we’ll get more into this in a moment but, you don’t have any formal wage loss report. If you’re making say $80,000 a year and you become injured and you can only make $50,000 a year. Well, simple math would say, “Well that’s $30,000 a year I’m losing let’s multiply that times ten or twenty and we’ve got a basic number there.” Well, economics doesn’t really work like that. Number one, you’re probably going to have a lot of fringe benefits that really can add up quickly for you. Number two is you don’t know that you’re necessarily going to make that $50,000 – could be a lot less. There are experts that get involved to calculate what you’re likely to make. And your lifetime expectancy can be pretty long. Your work-life expectancy. So those formal wage reports hired you know from experts there obtained from experts can really surprise you with how high those numbers can go.

Your Medical Options May Change

[25:17]: Next one is, it’s very important. You may have limited medical options or opinions about your future medical needs or life care plan. Medicals are a whole other category here that is very important with negotiating any type of injury case. The doctor you are – a lot of doctors, let me break this down as quickly as I can – a lot of doctors will be very reluctant to offer any kind of surgery. They really, there’s a whole school of doctors who will say, “Well that you might need this and it’s possible.” They like to use the word “possible.” Well, there are other doctors who are going to give you what I would call probably a more definite opinion and be a little more definitive as far as “Most likely you will need this.” Now you need to figure out pretty quickly what you’re actually going to need down the road.

Know Your Future Medical Costs

[26:10]: Anyway, the point is with the medical treatment you really need to figure out what you are going to need down the road – maybe five years, maybe even 10 years down the road – but chances are what are you going to need. And the other really important point is those surgery costs go up a lot each year. Medical expenses increase almost exponentially sometimes with the pharmacy increases in the surgery increases and hospital charges increasing. There are actual experts. We’ve done this on many, many cases: brain injury cases and catastrophic injuries, multiple surgeries. There is something called a “life care plan.” And what that is is it figures out if you need $4,000 in prescriptions today and each year. If you’re paying three or four thousand every year now for your prescriptions, you would be shocked at how high that will go over your lifetime and what that will end up meaning to you in terms of dollars. Same thing with the MRI every few years to monitor your back injury. Those costs go up every year. And when you multiply that over your life span, it gets very high very quickly. So when you start talking about even making the first offer you don’t know what those amounts really are going to be because you don’t have the experts involved at that point.

What if You Can’t Go Back to Work … Ever?

[27:32]: The third one here. And again I touched on this earlier in this is maybe a longer conversation I’m happy to have with anybody watching this if you want to call me. But basically a lot of times we see people who are injured, they sit out for a while, and they’re assuming they can go back to work when they talk about negotiating something. So in your head you may be thinking, “You know I feel decent, I haven’t had pain in a few months.” But you also have to think, “What have you been doing?” Have you actually been lifting 50, 80 pounds? Have you been working for 12 hours on your feet? Have you been up and down stairs all day? So you may be assuming that you can return to work, but you’re not really sure yet and you may be basing your idea of an offer on that.

Your Company May be Majorly at Fault

[28:15]: Fourth thing here is your company may be grossly at fault and they may have the records that prove it. And this got back and this goes back to what I suggest at the very beginning – to test their honesty. And you want to ask for all those key documents. If your company has all those key documents, and let’s say that this way you got injured was changed right afterward and they wrote it all up as being done horribly wrong, your company’s going to be very reluctant to go to court on a case like that. You need to know that when you sit down and try to start talking with them.

So you want to see with the information they have so you all are on an equal footing. If you make the first offer, you may not have those documents yet so you really don’t want to be shooting in the dark there.

How Would Your Settlement Change with an Attorney?

[28:58]: Final thoughts here, and let me go through this comparison. This may be the most valuable part of this webinar for you. How are things different with an attorney? And what I’m going to do now is, all those little points I made very quickly with you, I want to walk through them and give you a little comparison here. And this is going to help you understand the points and learn them better. But it’s also going to give you kind of an option B here on how things look different when a claim has been filed.

Seeing Your Injury from the Company’s Perspective

[29:25]: Let’s revisit the two most important things to a settlement. I mentioned this at the outset. The two tremendously important points are what is the possible value of your claim, and the other side’s always driven by what may happen if they don’t settle. Again, remember those two things. Those are from the other side’s point of view. And what I mean by that is what you really want to do is, and this is a good negotiation concept to begin with – but you want to sit in their chair so to speak. You really want to stand in their shoes. You want to think, “OK. Here I am. I’ve got this claim potentially that I’ve got to deal with. And what are the things that go through my head?”

[30:04]: The first thing probably is how bad could this claim be? What possible value could it be? What’s the highest value? The next thing that probably goes through the person’s head in that position is, “All right, how eager am I for a deal. What happens next month or next week if I don’t get this done?”

[30:20]: Let’s go through the possible value of your claim when you have an attorney. So again, put yourself in the seat of that insurance adjuster. Put yourself in the seat of that company claims guy. What is the value of your claim when you now have an attorney?

Louisiana Attorneys Can Pay for Medical Costs

[30:36]: Well you’re going to have this benefit. Certainly in Louisiana, for our clients, we pay for medical costs. We pay for testing because we need to know the full extent of our client’s injury so we can sit down and negotiate properly. So, you’re now going to have the benefit of having every test run, figuring out how bad your injuries are.

You’ll Have a Formal Wage Loss Report

[30:55]: You’re also going to have a formal wage loss report. We do this all the time for our clients. You’re going to know exactly what that 401K was worth. You’re going to know what those insurance benefits were worth. It’s another area that increases exponentially sometimes over the years. You’re going to know what your wage loss really is and you’re going to have an expert that we get these guys involved for all of our clients. You’re going to have basically a job expert to figure out what you are really going to make in that small town that you may live in.

You’ll Have Maritime Experts Testifying on Your Injury

[31:24]: We will hire, in almost all cases, we hire maritime experts and they can testify as to what the company may have done wrong. This becomes important because when the company’s evaluating your claim now, they’re looking at the full package. They now see the nature of your injuries and what the costs are going to be. They now see your financial losses in a report. They now see reports from experts saying what they did wrong and how your accident could have been avoided. They, the company, will now be faced with their own documents that we would have. That we can basically show them and then explain to them, “This is what happened. We now have all your documents; this is what the jury or the judge will see.”

The Company Will Have a Lawyer Working for Their Best Interests

[32:07]: Real important point here – this is the last one. They’re going to have a company lawyer involved. Once a claim gets filed in court, a lawyer will serve for the insurance company and they’re going to have a company lawyer involved who can tell or recommend to the insurance company what they should really pay to settle your claim. This is a high-level concept. When you are dealing unrepresented, when you’re not represented by a lawyer, and you’re dealing with an insurance adjuster; a lot of those guys are very very nice but they will have a limited ability to persuade the insurance company to pay high amounts of money to settle your case.

[32:47]: That is a very different situation. It’s a very different situation when a company attorney, an attorney hired by the insurance company who does maritime work who understands the potential value of the case, gets involved, looks everything over, maybe takes you to meetings with you, does depositions, hears our side of the case. That company lawyer can then go – and want to say he’s really a friend to you – but he can go do his job and he can go evaluate and recommend what they should pay you and a lot of times it’s many many multiples of what that adjuster might have offered you.

If They Don’t Settle When You are Represented by an Attorney

[33:23]: What happens to the other side if they don’t settle when you have an attorney? Now this gets to the second idea here. Again, one is the potential value of the case that drives what they’re going to offer. The second one is what happens if they’re not able to get a deal done. Well let’s look at what happens if they don’t settle when you have an attorney, when a claim has been filed for you.

The Company Continues Incurring Costs When They Don’t Settle

[33:48]: The best case is that the insurance company is going to keep paying their attorney. So, if we go in and we do a settlement meeting with them or a mediation, which is what we do all the time with our clients or sometimes courts will have settlement conferences, we go in on a Friday and we do a mediation and we’re not able to get a fair offer for our client, that case just keeps on going forward. And that insurance company knows that on Monday and Tuesday and Wednesday they’re going to be paying that attorney and they’re going to have to keep that file open and they’re incurring the cost. So there is a little bit of pain on their end if they don’t get a deal done in that sense.

The Company Will Be Under More Pressure to Settle

[34:25]: Another one here, another item is you will have people involved once a claim gets filed in court who have a real interest in trying to get things resolved, because that insurance adjuster and the company lawyer and the company itself – you know have kind of a triangle dynamic going on. Where kind of a simple way to say it is nobody really wants to look like a hero. Nobody on that end of the table who is going to want to stick their neck out and say, “You know, look. We know that this fellow went out. He got a lawyer. We know a lawyer has all these reports. We know his lawyer says the case could be worth $2,000,000, but we’re going to guarantee you he’s wrong and there’s no way he can possibly get that.” They’re just not going to stick their neck out and make 100% definitive declarations like that.

[35:17]: They are in a position where they need to start getting a lot more realistic about what could happen if a trial occurs or a judge puts a number on your case, puts his figure on it. That again, what I’m doing here, is comparing that to when you’re not represented. They don’t have any of that dynamic going on. When you’re not represented, it’s simply, “We couldn’t get a deal done with him. He didn’t take what we offered or he was too greedy,” and they move on and nothing bad happens the next week.

If They Don’t Settle, They Could Go to Trial

[35:48]: Worst case here. This is the last item, again critically important is they may face an upcoming trial date. And I have a saying I mentioned earlier and I say this all the time to our clients. When you get an electric bill or rent bill, do you ever go a month early and go pay that electric bill? Do you ever send the electric company money two months ahead of time? And say, “You know what. I know we haven’t even gotten a bill yet but we’re going to go ahead and prepay you. Because we think that down the road you’re eventually going to bill us, so we’re going to give you the money two months early.” People just don’t act like that. People would generally wait especially for – and this becomes even more important when it’s a higher-priced item or higher-ticket, higher-valued item. And in a case like yours may be, that could be very significant and worth a lot of money – people will wait until there is what I call a due date on that bill before they pay it.

[36:46]: And that trial date is, in a lot of ways, a due date for that company, that insurance company. If they don’t get your claim resolved by that trial date – or within a couple of weeks of it, maybe a month or two at the most – if they don’t get it resolved, you know coming up to that trial date, they got a due date. And if they’re wrong when they go to court, they may end up paying you a lot more than they could have. So that is critical and that is just a really important understanding they should have as to why it’s so powerful when you get a claim filed in court.

Their BATNA Changes When You Have an Attorney

[37:21]: Their alternative – and this is just a good way to summarize all this, again circling back to the core idea here that we’ve talked about. Their alternative if they don’t settle is now much, much different than before. When you’re sitting in a chair without a lawyer next to you and you’re trying to even entertain ideas about what your claim is worth, that is a real different environment. A real different world than when you’re sitting there with an attorney, you’ve got a trial date set, and you’ve got all those materials I talked about in your file. And you can tell the company this is what the claim will be worth to a jury or a judge and you guys need to come to the table.

Download the Webinar Summary

[37:57]: I would encourage you to download our free summary of these core ideas and concepts. Hopefully, this information has been helpful to you. I’m sorry we ran a little bit long. We have a lot of these webinars on our site here. We encourage you to look at them.

Get Help With Your Jones Act Injury Settlement

[38:11]: Please call us (504)-680-4100 if you have any questions about your particular situation. What I went through here, again, were just basic concepts and ideas. They may not necessarily apply to your situation. I would encourage you to call us if you have any questions at all. We truly enjoy helping injured maritime workers. We know how important it is to you all and hopefully this has been of help to you.